Cybercrimes have been increasing exponentially, with Ransomware being widely used to put companies in jeopardy. Financial losses incurred by companies have prompted the cybersecurity insurance market to expand as well.

According to statistics from security.org, the cybersecurity insurance market was valued at $7.8 billion in 2020, and the numbers are projected to grow to $20 billion by 2025. This data bears evidence that more companies racing to get their infrastructure insured. Cybersecurity premiums, however, are added costs that the company must invest in and can often take a toll on finances.

Keep reading as we suggest ways to reduce cybersecurity insurance premiums throughout this comprehensive guide.

What is cybersecurity insurance?

Cybersecurity insurance, also known as cyber insurance or cyber risk insurance, is a specialized form of insurance designed to protect businesses and individuals from the financial consequences of cyber threats and attacks. This type of insurance typically covers expenses related to data breaches, hacking incidents, and other cybercrimes, offering financial compensation for losses such as data recovery, legal fees, and notification costs.

Cybersecurity insurance is an important factor in the digital age, where the frequency and sophistication of cyber attacks continue to go up. It provides a safety net for organizations and individuals, helping them tackle the financial impact of cyber incidents and encouraging proactive cybersecurity measures. As the threat landscape evolves, cybersecurity insurance remains vital in enhancing overall risk management strategies in an increasingly interconnected and technologically reliant world.

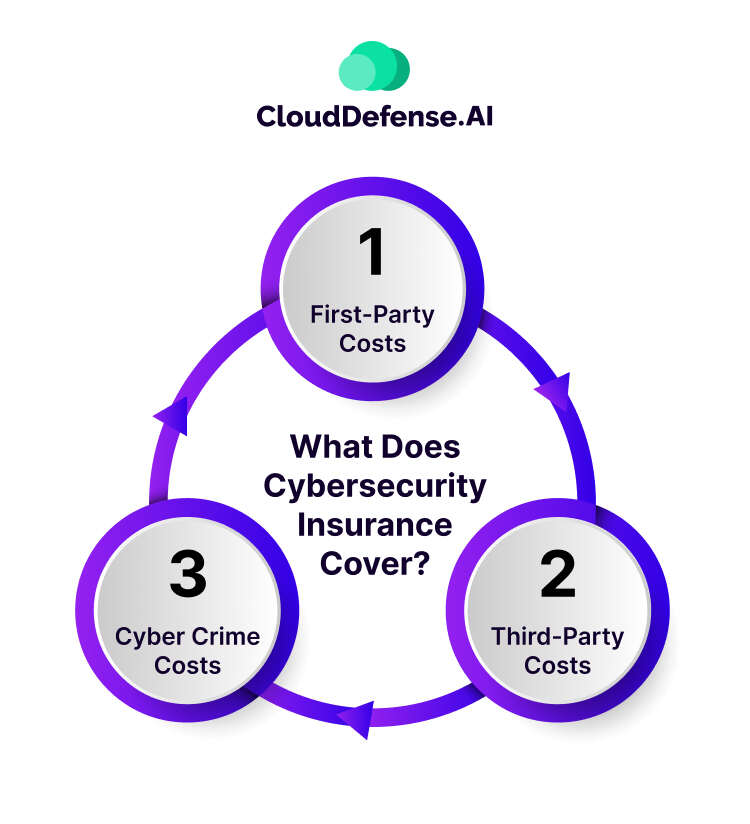

What does cybersecurity insurance cover?

Cyber insurance comprehensively addresses three key types of expenses to mitigate the financial impact on organizations.

First-Party Costs

First-party coverage concerns expenses incurred by the insured organization to minimize the impact of a cyber incident or data breach. This includes services such as public relations to manage company reputation, notification of affected parties, and engaging incident response and recovery services.

First-party coverages not only include alerting affected parties, and implementing PR campaigns for reputation management, but also provide assistance with credit monitoring, and undertaking recovery and remediation efforts. Common insurable events falling under first-party coverage involve destroying data by malicious parties, malware infections, DoS attacks, ransomware incidents, and damage to computer hardware due to natural calamities.

Third-Party Costs

Third-party coverage addresses cyber liability for firms responsible for a client’s online security. It covers legal fees if a client sues the company for a data breach. Third-party insurance includes costs such as lawyers’ fees, settlements or judgments, and miscellaneous court expenses like witness and docket fees.

This coverage is crucial for businesses that secure customers’ online data, such as IT consultants, software developers, app developers, network and security consultants, and web hosting companies.

Cyber Crime Costs

This category covers financial losses directly resulting from cybercrimes. Notable examples include ransom fees arising from a ransomware attack. Cybercrime coverage ensures businesses can navigate and recover from the financial aftermath of malicious online activities.

Understanding and securing these comprehensive coverage types is essential for businesses operating in today’s digital landscape, where cyber threats are prevalent and potentially devastating.

What cybersecurity insurance doesn’t cover?

Cyber insurance often excludes coverage for specific expenses and scenarios.

Technology Upgrades

Cyber insurance may not cover costs associated with enhancing internal technology or upgrading systems post-cyber incident. Businesses seeking to bolster their cybersecurity infrastructure may need to bear these expenses independently.

Future Lost Profits

Cyber insurance typically doesn’t cover potential future profit losses resulting from a data breach. It addresses immediate and tangible damages rather than speculative or projected financial impacts.

Valuation Loss

If intellectual property theft leads to a decline in company valuation, this decrease may not fall under the coverage umbrella of cyber insurance. Valuation losses are often excluded from standard policies.

Dishonest Conduct

Withholding information from the insurance company during the policy purchase can lead to the exclusion of losses. Full and transparent disclosure is crucial to ensure the validity of claims.

Unauthorized Data Collection

Cyber insurance may not cover losses incurred due to illegitimate data collection practices. Policies typically emphasize protection against external cyber threats rather than internal data mishandling.

Understanding these limitations is essential for businesses when assessing their cyber insurance coverage. It emphasizes the importance of aligning insurance policies with specific organizational needs and risk profiles. Regular policy reviews, open communication with insurers, and adherence to cybersecurity best practices remain crucial in navigating the evolving landscape of cyber threats.

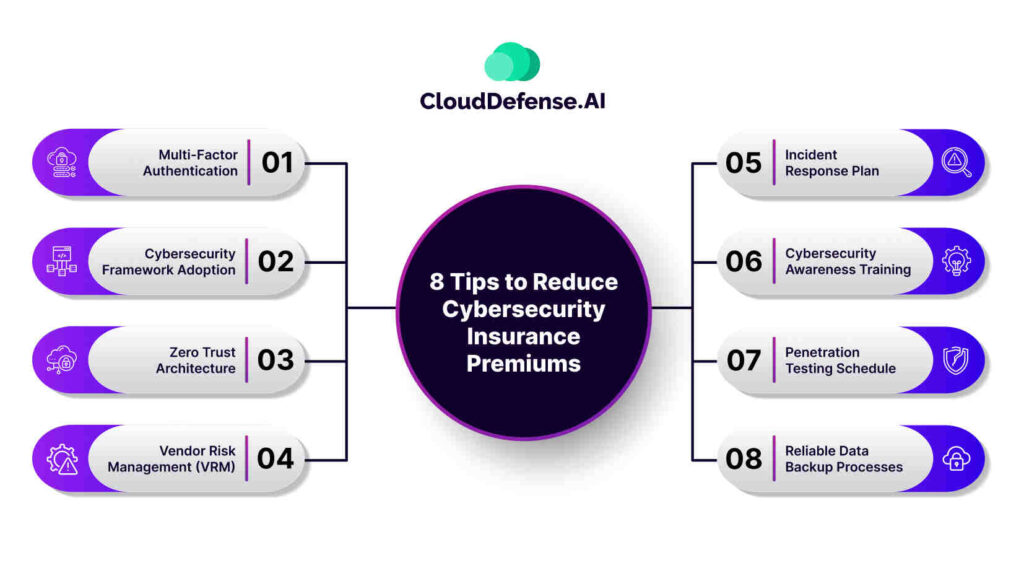

8 Tips to Reduce Cybersecurity Insurance Premiums

Building a powerful cybersecurity program strengthens your defenses and can help reduce cybersecurity insurance premiums. By combining the following strategies, you can enhance your cybersecurity posture and align with the criteria that insurers evaluate when assessing risk.

Multi-Factor Authentication

Enforce Multi-Factor Authentication (MFA) as a crucial security measure to thwart credential theft. Additionally, explore passwordless MFA solutions using biometrics for heightened security and an improved user experience, ensuring a resilient defense against unauthorized access.

Cybersecurity Framework Adoption

Demonstrate a dedication to cybersecurity enhancement by adopting frameworks such as NIST Cybersecurity. Develop a documented pathway illustrating ongoing initiatives for continuous improvement, reinforcing a commitment to strong cybersecurity practices.

Zero Trust Architecture

Demonstrate a proactive defense stance by adopting a zero-trust model, which is particularly crucial for remote workforces. Align your approach with recognized standards like NIST 800-207 to ensure a comprehensive and effective zero-trust security model implementation.

Vendor Risk Management

Effectively manage third-party risks by implementing a Vendor Risk Management (VRM) program that continuously monitors security within the supply chain. Enhance proactive security measures by incorporating an attack surface monitoring feature, swiftly detecting and addressing misconfigurations to bolster overall cybersecurity resilience.

Incident Response Plan

Minimize the impact of potential breaches by developing a thorough incident response plan. Demonstrate your preparedness to insurers by presenting a well-documented, comprehensive document that outlines effective strategies for responding to and mitigating the consequences of cybersecurity incidents.

Cybersecurity Awareness Training

Maintain staff vigilance against cyber threats through regular training and simulated phishing attacks. Ensure employees are equipped to recognize and respond adeptly to common cyberattack tactics, fostering a resilient and security-conscious workforce.

Penetration Testing Schedule

Highlight the adaptability of your cybersecurity defenses by regularly conducting penetration tests. Demonstrate a proactive approach to addressing evolving threat landscapes, reinforcing a commitment to staying ahead of potential security challenges.

Reliable Data Backup Processes

Ensure resilience against ransomware attacks by establishing data backup and loss prevention solutions. Implement best defense strategies, such as regular security solution updates and a comprehensive business continuity plan, to safeguard against and recover from potential cyber threats effectively.

Implementing these measures not only enhances your cybersecurity resilience but also positions your business favorably in the eyes of insurers, potentially leading to lower cyber insurance premiums.

Cybersecurity Insurance for Critical Infrastructure and Industrial Sectors

The dynamic evolution of the cyber threat landscape poses heightened risks to critical infrastructure, including energy, transportation, and healthcare sectors. With emerging technologies expanding the attack surface, the sixteen vital categories of US critical infrastructure become prime targets for cybercriminals.

Despite financial services, healthcare, IT, transportation, and communications accounting for 40% of cyber activity, these organizations managing critical infrastructure have been slow to fortify against these threats. Recognizing that 95% of breaches stem from IT failure or human error and 28% from destructive attacks, the necessity for effective cybersecurity measures is clear.

FAQ

How much does cyber security insurance cost?

The cost of cybersecurity insurance varies based on factors such as the size of the business, industry, coverage needs, and risk profile. Small businesses may pay a few thousand dollars annually, while larger enterprises might face higher costs, often ranging from $10,000 to $100,000 or more per year.

Is cybersecurity insurance worth it?

Yes, cybersecurity insurance for businesses is worth it. It provides financial protection against the potentially devastating costs of cyberattacks, helping cover expenses like legal fees, notification costs, and system repairs. It enhances overall resilience and aids in mitigating the impact of security incidents.

Does cyber insurance reduce risk?

Cyber insurance itself doesn’t directly reduce the risk of cyber incidents. Instead, it provides financial protection and support in the aftermath of an incident. To reduce risk, a comprehensive cybersecurity strategy, including preventive measures and risk management practices, is crucial alongside cyber insurance.

Which of the risk management strategies would cybersecurity insurance be used?

Cybersecurity insurance is part of the risk transfer strategy in risk management. In this approach, businesses transfer a portion of their financial risk associated with cybersecurity incidents to an insurance provider. This helps mitigate the financial impact of potential breaches and supports recovery efforts.

Conclusion

As cyber threats multiply, cybersecurity insurance becomes mandatory for businesses seeking financial protection against the repercussions of cyberattacks. While costs are a consideration, implementing strong cybersecurity practices fortifies defenses and contributes to lower insurance premiums.

Businesses must align their insurance coverage with specific needs, regularly review policies, and adopt proactive risk management strategies to navigate the cyber world’s complexities successfully. We hope this article aids you in your quest to reduce cybersecurity insurance premiums.